Taxes 2023: Credits, deductions and tax breaks for student loans and college costs

Grants, scholarships and financial aid are all useful for handling the very real costs of a college education, but don’t sleep on tax credits and deductions. Both college students and parents of college students can take advantage of tax breaks that can mean thousands of dollars of savings on tuition, fees, books, and supplies.

Here are some of the best college-related tax credits, deductions and other tax breaks that you may be able to take.

American Opportunity Tax Credit

The American Opportunity Tax Credit allows you to lower your income tax bill by up to $2,500 per student, per year on undergraduate tuition, fees and books. Room and board, though, don’t count.

“But you can only claim this tax credit for the first four years of higher education,” said Meagan Landress, a student loan consultant for Student Loan Planner. To claim the credit, fill out IRS Form 8863 with your tax return.

Who qualifies: Undergraduate college students who file their own tax returns or parents who pay the college tuition costs for children listed as dependents on their tax return qualify for the credit.

To earn the credit, your modified adjusted gross income (MAGI) must be below $80,000 if you are filing your tax return as single or as head of household or less than $160,000 if you are filing jointly. You can also get a reduced credit if your MAGI is between $80,000 and $90,000, as a single filer/head of household or between $160,000 and $180,000 as a joint filer. You can calculate your MAGI here.

Lifetime Learning Credit

The Lifetime Learning Credit is similar to the American Opportunity Tax Credit, but structured differently. It allows you to claim 20% of the first $10,000 you paid for tuition and fees in the previous year. Once again, tuition, fees, books and equipment count, but room and board don’t.

The Lifetime Learning Credit, though, isn't just for undergrads, but also graduate and vocational students, too. There’s also no limit to the number of years that you can claim the credit. You can also only claim one of those two education tax credits in the same year. To claim the Lifetime Learning credit, fill out IRS Form 8863 with your tax return.

Who qualifies: Undergraduate, graduate, or vocational college students who file their own tax returns or parents who pay the tuition of a child they claim as a dependent qualify.

The financial requirements for the Lifetime Learning Credit are the same as for the American Opportunity Tax Credit. Your modified adjusted gross income (MAGI) must be below $80,000 if you are filing your tax return as a single filer or as a head of household or less than $160,000 if you are filing jointly. You can also get a reduced credit if your MAGI is between $80,000 and $90,000, as a single filer/head of household or between $160,000 and $180,000 as a joint filer.

Student Loan Interest Deduction

Do you pay interest on a student loan? Then you might be able to deduct up to $2,500 worth of the interest you paid for either a federal or private student loan — or both. You can claim the deduction on your federal income tax return, Form 1040.

Who qualifies: Anyone who paid interest on a qualified student loan in the eligible tax year is eligible as long as they are not claimed as a dependent on someone else’s tax return. For 2022 taxes, the full deduction is available to a single or head-of-household filer with a MAGI less than $70,000 or less than $145,000 for a joint filer. The deduction is reduced for single or head-of-household filers making between $70,000 and $85,000 or between $145,000 and $175,000 for joint filers. Married people who file separately are not eligible for the deduction.

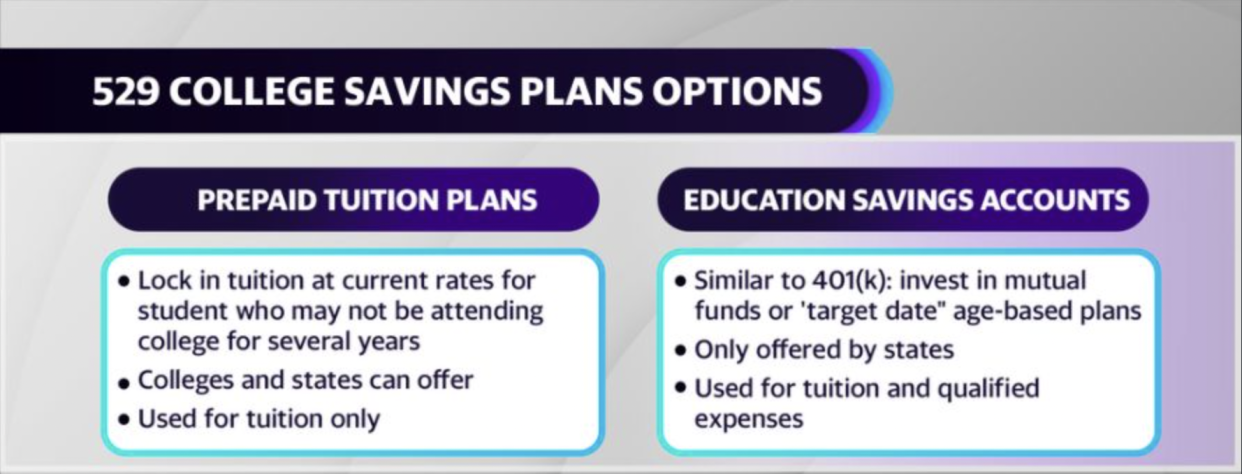

529 Savings Plan

529 Plans, which are available in every state, can be a great way to stash away cash for college expenses. That’s because these plans have major tax advantages, Landress said, including:

Tax-free growth: Earnings grow free from federal and state income tax.

Tax-free withdrawal: Any money you use from the fund on qualified education expenses like tuition or books aren’t taxed on the state or federal level.

State tax deduction or credit: Depending on which state you live in, you could be eligible to claim a 529 tax deduction for making contributions to the plan.

There are two types of 529 plans: a prepaid tuition plan, which lets you buy tuition credits at today’s prices for future enrollment in a given school, and an education savings plan which allows you to open a tax-advantaged account to save money for school expenses. Those expenses can even include computer equipment and reasonable room and board, said Tracie Miller-Nobles, a certified public accountant and a lead faculty member in the accounting department at Franklin University.

The funds in a 529 plan can also be used to pay off student loans although there are some limitations, including a $10,000 lifetime withdrawal limit. You can use money in a 529 plan for non-education-related expenses, but those distributions are taxable and you’ll be hit with a 10% penalty, too, Miller-Nobles said.

Who qualifies: Anyone can open and contribute to a 529 plan for themselves or for someone else.

“These plans are a great way to set aside money for college,” Miller-Nobles said. “I especially encourage parents of young children to consider investing in a 529 plan.”

Kate Rockwood is a freelance writer and editor.

Click here for the latest economic news and economic indicators to help you in your investing decisions

Read the latest financial and business news from Yahoo Finance

Download the Yahoo Finance app for Apple or Android

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube.

Source: Read Full Article