Budget will reduce need for increases in interest rates

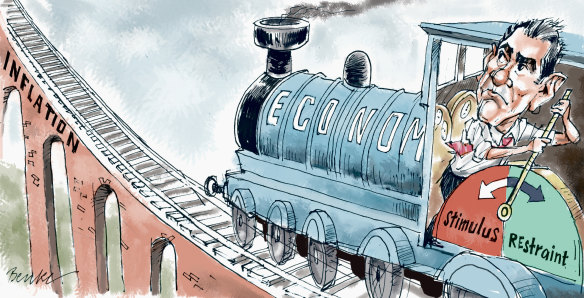

When the economy’s needs have switched from stimulus to restraint, it helps to get in new economic managers, who can reverse their predecessors’ direction with zeal rather than embarrassment.

The need for economic policy to change course became clear only during this year’s election campaign, when the Reserve Bank’s concern about rapidly rising inflation prompted it to make the first of many rises in the official interest rate.

Treasurer Jim Chalmers is trying to get the budget deficit as low as possible which he hopes will reduce the need for many more interest-rate increases.Credit:Alex Ellinghausen

So this week’s second go at a budget for the present financial year was needed not just to accommodate a new government with different policies and preferences, but to change the budget’s direction from push-forward, to pull-back.

In just those few months, we changed from “gee, aren’t we roaring along” to “gosh, we better slow down quick”. One moment we’re seeing how low we can get the rate of unemployment, the next we’re jacking up interest rates in a struggle to get inflation down.

A drawback of living in a market economy is that it moves through a “business cycle” of alternating boom and bust. The role of the economic managers is to “stabilise” – or smooth out – the demand for goods and services, cutting off the peaks and filling in the troughs.

The problem with booms is that as demand (spending) starts running ahead of supply (production), it pushes up prices and the inflation rate. The problem with troughs is that as demand falls behind supply, businesses start sacking workers and unemployment rises.

The macro managers use two “instruments” to smooth the cycle’s ups and downs: the budget (“fiscal policy”) and interest rates (“monetary policy”).

With the budget, they increase government spending and cut taxes to add to demand and so reduce unemployment. They cut government spending and increase taxes to reduce demand and so reduce the rate of inflation.

With interest rates, the Reserve Bank cuts them to encourage borrowing and spending by households, so as to reduce unemployment. It increases them to discourage borrowing and spending by households and so reduce inflation.

So, which of the two policy levers should you use?

A new conventional wisdom has emerged among top American academic economists that, because of the two levers’ contrasting strengths and weaknesses – and because interest rates are so much closer to zero than they used to be – you should use fiscal policy to boost demand, but monetary policy to hold it back.

Credit:Joe Benke

This more discriminating approach has yet to become the accepted wisdom, however. The old wisdom is that monetary policy is the better tool to use for both stimulus and restriction.

The budget’s “automatic stabilisers” (mainly bracket creep and unemployment benefits) should be free to help monetary policy in its “counter-cyclical” role, but discretionary, politician-caused changes in government spending and taxes should be used only in emergencies, such as recessions.

So expansionary fiscal policy did much of the heavy lifting during the pandemic – hence the huge budget deficits and addition to government debt.

But now the Reserve and monetary policy have taken the lead in slowing demand within Australia, so it doesn’t add to the higher prices we’re importing from abroad, thanks to the pandemic-caused supply chain disruptions and the Russian-war-caused leap in fuel prices.

The conventional wisdom also says that, whatever you do, never have the two policy tools pulling in opposite directions rather than together.

If you’re mad enough to have the budget strengthening demand when the independent central bank wants it to weaken, all you do is prompt the bankers to lift interest rates that much higher. This is the “monetary policy reaction function”. One way of saying the central bankers always have the trump card.

Which brings us to this week’s budget redux. How did Treasurer Jim Chalmers play his cards? He did what he thought he could to get the budget deficit as low as possible and so back up monetary policy’s efforts to reduce demand. He’s no doubt hoping this will reduce the need for many more interest-rate increases.

First, Finance Minister Katy Gallagher hacked away at the Morrison government’s new spending programs, so that Labor’s promised new spending could take their place with little net addition to expected government spending over this financial year and the following three.

This wasn’t particularly hard because most of the Coalition’s plans were politically driven, and most hadn’t got going before government changed hands in May.

Second, the same attack on Ukraine that’s causing household electricity and gas bills to rocket has also caused the profits of Australian gas and coal exporters to rocket, along with their company tax bills.

As well, the Coalition’s success in getting employment up and unemployment down has caused a surge in income tax collections.

This huge boost to government revenue isn’t expected to last, so Chalmers has decided to “bank” almost all of it rather than spend it. That is, use it to reduce the budget deficit.

The conventional wisdom also says that, whatever you do, never have the two policy tools pulling in opposite directions rather than together.

The budget in March expected a budget deficit for the year to this June of $80 billion. Thanks mainly to the tax windfall, it came in at $32 billion, a huge improvement, equivalent to more than 2 per cent of gross domestic product.

The deficit for this year was expected to be $78 billion, but now $37 billion is expected, an improvement of almost 2 per cent of GDP. Next financial year, 2023-24, has gone from $57 billion to $44 billion.

So, the budget deficit is expected to fall continuously from a peak of $134 billion (6.5 per cent of GDP) in 2020-21 to $37 billion (1.5 per cent) this financial year.

That’s enough to convince me the “stance” of fiscal policy is now restrictive. I reckon it’s also enough to convince Reserve Bank governor Dr Philip Lowe that fiscal policy is co-operating in the effort to restrain demand and control inflation.

One small problem. After this year, the deficit’s projected to start drifting back up, and stay at about 2 per cent of GDP until at least 2032-33.

Oh dear. Why? Tell you next week.

Ross Gittins is the economics editor.

The Business Briefing newsletter delivers major stories, exclusive coverage and expert opinion. Sign up to get it every weekday morning.

Most Viewed in Business

From our partners

Source: Read Full Article